The offer hit your inbox at $1.2M. You read the number. You did not read the terms. Three months later you closed at $940k and never fully understood where the rest went.

That gap usually lives inside one document. Every letter of intent app sale looks harmless, often just a single page. But five terms buried inside it decide how much of that headline number actually reaches your account.

Most founders sign on the price alone. The buyer is counting on exactly that. The LOI is short on purpose. It moves fast, it feels like progress, and it quietly sets the rules for everything that follows in the purchase agreement.

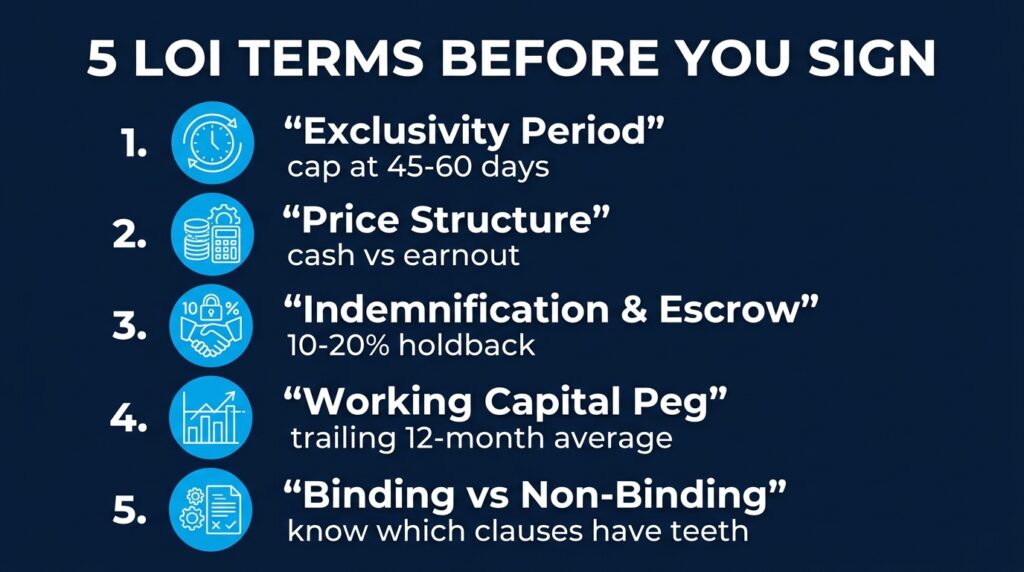

Here are the five terms that move the money.

Term 1: The Exclusivity Period (No-Shop)

The moment you sign, the clock starts. Exclusivity, sometimes called a no-shop clause, means you stop talking to every other buyer for a set window. Most run 60 to 90 days.

That sounds fair until you see what it does to your leverage. Once you are locked in, the only buyer at the table is the one who just told you to stop looking. Re-trades happen here. The price drifts down because you have no one else to call.

Cap the window. For an app with clean books, 45 to 60 days is plenty. Tie the clock to the buyer actually starting due diligence, not to the day you signed.

Term 2: How the Price Is Actually Structured

A $1M offer is not $1M if half of it is an earnout. The structure line tells you how much is cash at close, how much is seller financing, and how much rides on hitting future targets.

Earnouts are common and getting more so. Roughly 60% of software deals now include an earnout tied to revenue or retention over 12 to 18 months. That is money you only see if the app performs after you have handed over the keys.

Push for cash. If an earnout stays, tie it to revenue, not profit, and to metrics you still control. An earnout pegged to a number the buyer manages is a number the buyer can shrink. The type of buyer across the table shapes the structure they offer, which is the same reason two buyers can be $180k apart on the same app.

Term 3: Indemnification and the Escrow Holdback

This is the term founders skip and regret in a letter of intent app sale. Indemnification sets how long the buyer can come back at you after closing and how much they can claw back. Part of your price gets parked in escrow until that window closes.

Holdbacks usually run 10% to 20% of deal value, released over 12 to 18 months. On a clean app with documented numbers, that figure should compress toward the low end.

Read three things: the cap (the most you can lose), the survival period (how long claims stay open), and the basket (the minimum before a claim counts). Vague language here is expensive later.

A clean app shortens all three. Documented revenue, clear app store accounts, and no surprise chargebacks give you the case to argue the holdback down and the survival window shorter. The messier your books, the more of your own money the buyer gets to sit on.

Term 4: The Working Capital Peg

Apps carry working capital too. Prepaid ad spend, outstanding receivables from the app stores, deferred revenue from annual subscriptions. The working capital peg sets the baseline you are expected to deliver at close.

Buyers usually peg it to a trailing 12-month average so you cannot drain the account before handover. Fair enough. The trap is a vague peg. If the LOI does not define what counts, you end up negotiating it mid due diligence, from a weaker seat, after exclusivity has already locked you in.

Get the number, or at least the formula, into the LOI before you sign.

Term 5: What Is Binding and What Is Not

Most of the LOI is non-binding. The price is not a promise. But a few clauses bind you the second you sign: exclusivity, confidentiality, and who eats the cost if the deal dies.

Founders assume the whole document is a soft handshake, then discover the exclusivity clause is fully enforceable while the price was never guaranteed at all. Know which lines have teeth before you put your name on them.

What Every Letter of Intent App Sale Comes Down To

A letter of intent app sale is where the deal is really priced. The headline number gets you to the table. These five terms decide what you actually walk away with.

You do not have to read them alone. We fight for price and terms. Before you sign anything, see what the full sale process looks like, then put your LOI in front of someone who has read a few hundred of them.

Planning your exit? Have us pressure-test your LOI before you sign anything.

FAQ

Is a letter of intent app sale binding? Mostly no. Price and structure are usually non-binding placeholders. The exclusivity and confidentiality clauses are the parts that bind you the moment you sign, so read those first.

How long should the exclusivity period be? For an app with clean books, push for 45 to 60 days and tie the clock to the start of due diligence. Ninety days hands the buyer a long runway to re-trade while you sit with no other options.

Can I still negotiate after signing the LOI? Yes, but from a weaker seat. Anything left vague in the LOI gets settled during due diligence, after exclusivity has already removed your other buyers. The more you pin down up front, the less leverage you give away.